In this article:

- Item J- PSI cannot be negative

- Net PSI Loss

- Amendments relating to personal services income

- Net PSI loss reduces overall table income. i.e. there is no carried forward loss

- What if not qualify as PSI?

- Section 86-27 - Conditions

- Rules apply to PSI income loss

- How to report deferred non-commercial business losses

- Operates directly as a sole trader under their own ABN

Item J- PSI cannot be negative

Amounts in PSI section should not be negative. It is mandatory for ATO and cannot be avoided. Negative amount can be entered in table item, but only to adjust total value. The amount of field still should be positive.

Net PSI Loss

The individual can use the loss to offset against their other income OR if they do not have enough other income, then the overall loss (other income-PSI-deductions = some negative value) will be carried forward.

The individual will have a normal carried forward loss.

Note: PSI loss reduce the overall taxable income.

Amendments relating to personal services income

The Schedule also amends the personal services income provisions in Part 2-42 of the ITAA 1997 to ensure that an individual, working through a personal services entity, can deduct a net personal services income loss in an income year. Learn more

Net PSI loss reduces overall table income. i.e. there is no carried forward loss

Illustration: Net PSI loss reduces overall table income. i.e. there is no carried forward loss.

What if not qualify as PSI?

If the personal services entiy has made a net PSI loss, the individual is entitled to a deduction for the loss. Learn more from the ATO

Section 86-27 - Conditions

Rules apply to PSI income loss

Illustration: Do the rules ie, minimum of 20,000 apply to Personal income loss?

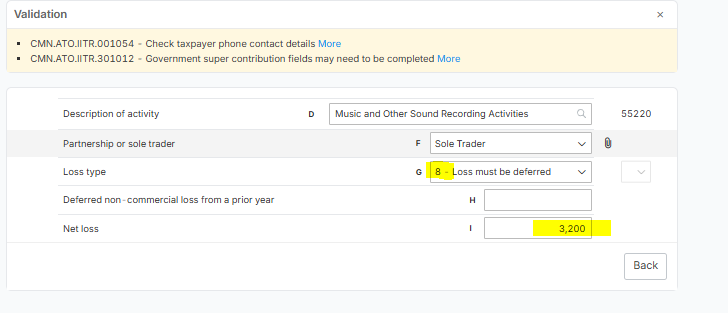

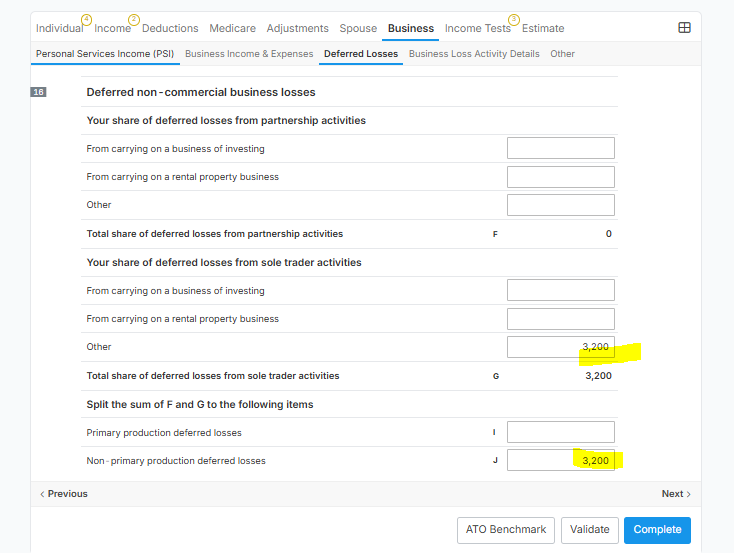

How to report deferred non-commercial business losses

How to report deferred non-commercial business losses

Lodge a Business and Professional Items Schedule 2024: Before completing the supplementary tax return, ensure you have lodged a Business and Professional Items Schedule 2024. This is necessary to report deferred non-commercial business losses.

Record Deferred Losses:

- For losses from business activities conducted in partnership, write the total of your net losses to be deferred at question 16 – label F.

- For losses from business activities as a sole trader, write the total of your net losses to be deferred at question 16 – label G.

Operates directly as a sole trader under their own ABN