The reconciliation section of a tax return allows the accounting income to be reconciled to the taxable income. The reason for this is that certain income items may not be assessable or the amounts may differ. Similarly, with expenses, some accounting amounts may not be deductible or amounts may differ.

Understanding the Reconciliation Section

The reconciliation section will only be relevant if you've imported financial statements.

LodgeiT forms are optimised for autofill from downstream accounting systems, not manual fill processes.

LodgeiT Reconciliation demonstrates how tax facts are arrived at from accounting facts.

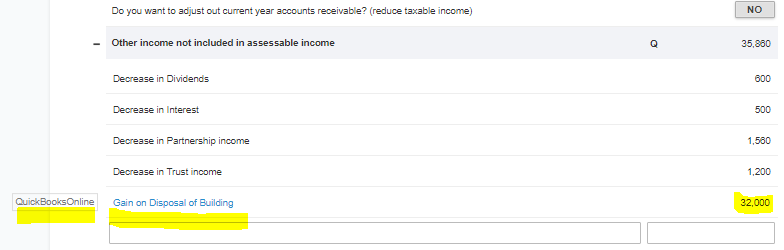

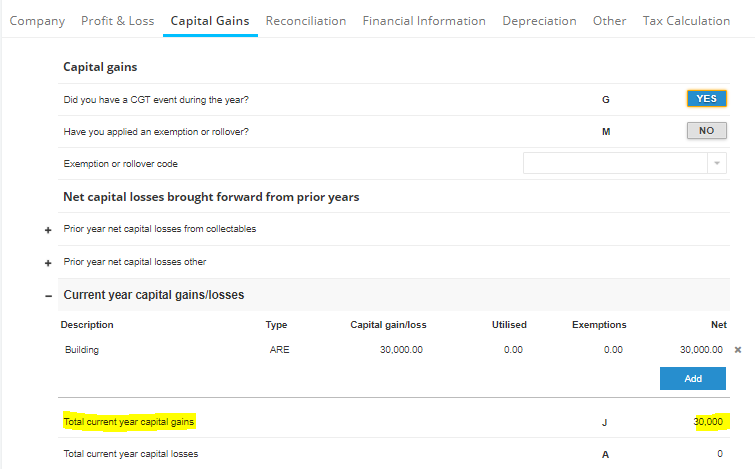

Note the Add: Net capital gain at 7A and Less Other Income not Included in Assessable Income accounting representation of the capital gain - Gain on Disposal of a Building.

Click here for SBE depreciation

This is where 7A Taxable Capital Gain is coming from the capital gains section of the form.

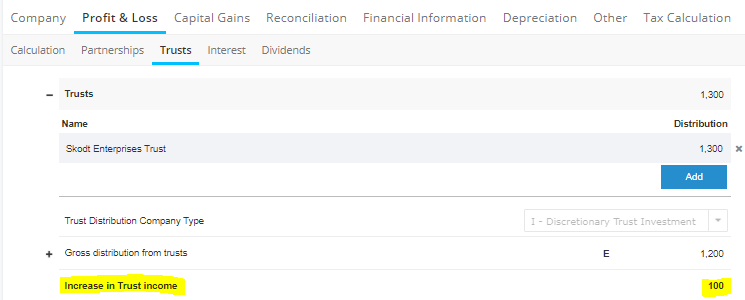

Other Assessable Income used to report an increasing adjustment in Trust Income. Any increasing adjustment in dividend, partnership or interest income will be reflected in the same manner.

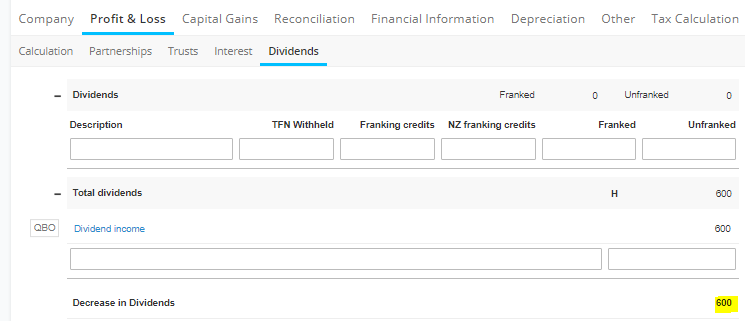

Other Income not included in Assessable Income used to report a decreasing adjustment in dividend income. . Any decreasing adjustment in trust, partnership or interest income will be reflected in the same manner.

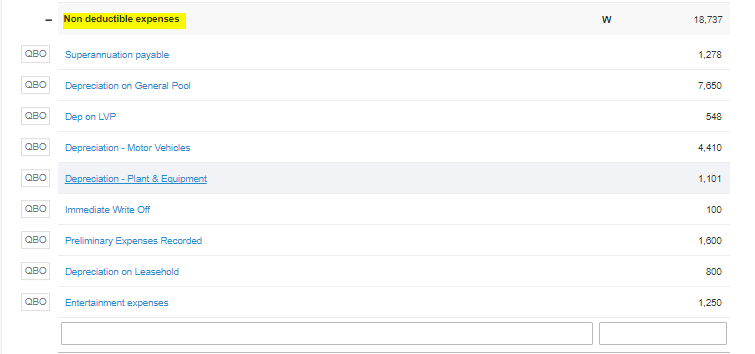

Non Deductible Expenses

The general rule is that all accounting depreciation is treated as non deductible. Your reportable taxable deductible depreciation facts will be included either from the LodgeiT Depreciation calculators or from the depreciation tab of the company tax form. This same method is used for -

- Capital allowance assets

- Capital works assets

- Immediate write off assets

- Preliminary expense/blackhole/Sec 40-880

Click here to learn more about Small Business (SBE) non deductible

Non deductible superannuation with the mouse hovering over the line item, shows that it is coming from the current year balance sheet i.e. the superannuation liability.

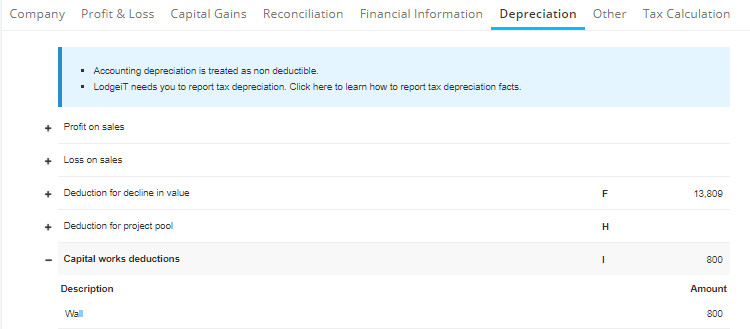

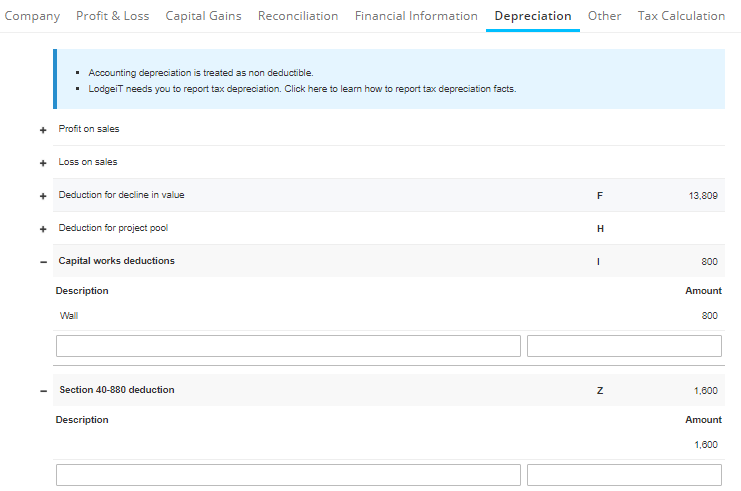

For Less depreciation, the taxable deductible value shows in the reconciliation section at 7F.

The deductible depreciation is captured either from -

a. The LodgeiT Depreciation Calculators

b. A manual fill

Accounting capital works are added back in the 'non deductible' section and then the taxable reportable fact is reflected at 7i

The deductible capital works is captured either from -

a. The LodgeiT Depreciation Calculators b. A manual fill

Any accounting-related expenses that are non deductible need to be tagged accordingly.

Non deductible entertainment in the non deductible expense section.

If you explore to Accounts section, where classifications are carried out, you'll find that the entertainment expense line item has been tagged as non deductible.

Deductible Capital works & Section 40-880 expenses reflect in the Less: section of the reconciliation section. Both tax deductible values arrive from the Depreciation section either automatically via the depreciation module or via a manual input. Example below is the automatic variant.

Related Article: