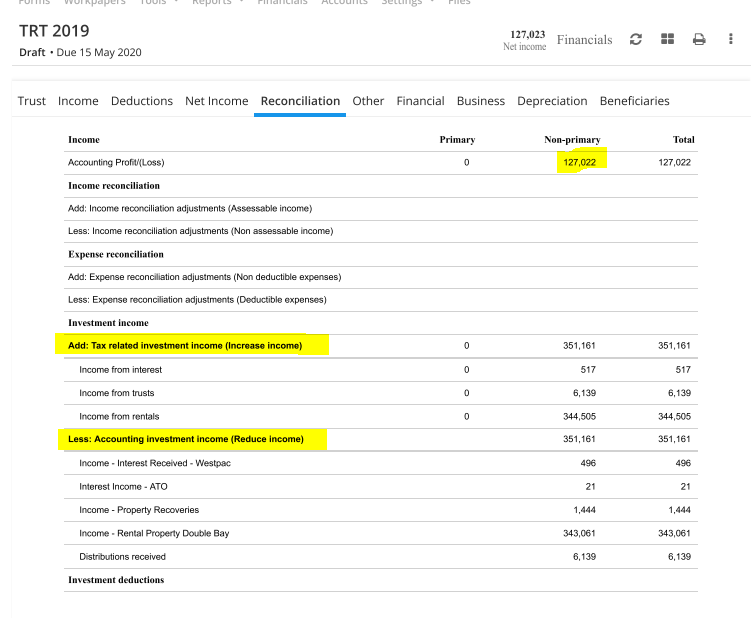

The reconciliation section in the Trust tax return 2025 bridges accounting profit (or loss) to taxable income at item 65. Differences occur because certain income items (e.g., exempt or foreign) are non-assessable, while others (e.g., grossed-up franked dividends) exceed accounting figures under AASB standards. Similarly, expenses like depreciation or entertainment may not be fully deductible or differ under ITAA 1997 tax rules.

Reconciliation Explanation

Accounting profit often differs from taxable income due to varying treatments, especially for investment income like franked dividends or partnership distributions. LodgeiT's Reconciliation tab automatically backs out accounting figures and adds tax-adjusted amounts per ITAA 1997 and ATO Trust tax return 2025 instructions, ensuring accurate net income at item 65.

Example 1:

Example 2:

Enter adjustments in the Income or Expenses tabs.

they flow automatically to the Reconciliation tab for review.

Verify totals match your worksheets before lodgement. All trusts (except AMITs, CCIV sub-funds, public trading trusts) must complete this.

For SBE, click here - Simplified Depreciation Rules "Depreciation Expenses on Accounts"

Related Article:

Trust Income Earned by a Trust